Dental HMO vs. PPO for Practices (June 2026)

HMO vs. PPO dental billing explained for practices in June 2026. Compare capitation checks, claim workflows, reimbursement rates, and cash flow timing.

Max Shore - July 6, 2026

Dental HMO vs PPO sounds like a simple network choice until you realize one pays you per claim and the other pays you per member, regardless of who shows up. PPO dental insurance means submitting a claim for every cleaning, filling, and crown, waiting weeks for the carrier to adjudicate, and writing off the gap between your fee and the contracted allowable. Under an HMO, you get a monthly capitation payment for each assigned member, collect fixed copays at each visit, and skip most claims entirely. If you're comparing the best PPO dental insurance carriers, weighing dental PPO vs HMO cost, or wondering whether Cigna dental HMO vs PPO Reddit threads actually help, the real question is how each plan type changes your billing team's workload and your cash flow timeline. Credentialing takes the same 60 to 180 days for PPO dental insurance providers like Cigna, Aetna, Blue Cross Blue Shield, and Anthem, or for HMO panels, but once you're in-network, the revenue mechanics look nothing alike. From eligibility checks and claim workflows to patient collections, attachment requirements, and what buyers see when they model your EBITDA, we'll walk through what independent practices actually need to know about billing under each model in 2026.

TLDR:

- DHMO plans pay your practice a monthly capitation check per member, while PPO plans reimburse per procedure at 20-40% below UCR rates.

- DPPO claims take 14-45 days to pay, while DHMO capitation arrives monthly regardless of patient visits.

- Credentialing with Cigna, Aetna, or BCBS takes 90-180 days before you can bill in-network rates.

- Heavy DHMO payer mix lowers practice valuation multiples; balanced PPO with 25%+ fee-for-service commands premium prices.

- Lassie automates EOB retrieval and posts line-item payments into Dentrix, Eaglesoft, or Open Dental against contracted fee schedules.

Understanding HMO and PPO Dental Plans: Core Definitions

Dental HMO and PPO plans share an acronym lineage with their medical cousins, but the billing mechanics sit in different worlds. A DHMO (sometimes DMO) operates on a capitation basis: the carrier pays a contracted dentist a fixed monthly per-member fee, whether the patient visits twice a year or never. A DPPO works on a fee-for-service basis inside a negotiated fee schedule, where each procedure code triggers reimbursement at the contracted allowable rate.

DHMO at a glance

- Patients select a primary dental office from the carrier's network

- The practice receives a monthly capitation check regardless of utilization

- Preventive care carries little or no patient copay

- Specialty referrals route through the assigned provider

- Out-of-network care is generally not covered

DPPO at a glance

- Patients can see any licensed dentist, with higher benefits in-network

- The carrier pays a percentage of the contracted fee per procedure

- Annual maximums, deductibles, and waiting periods apply

- Submitted claims drive every payment event

- Out-of-network visits still receive partial reimbursement at a reduced rate

How Each Plan Type Affects Practice Revenue and Reimbursement

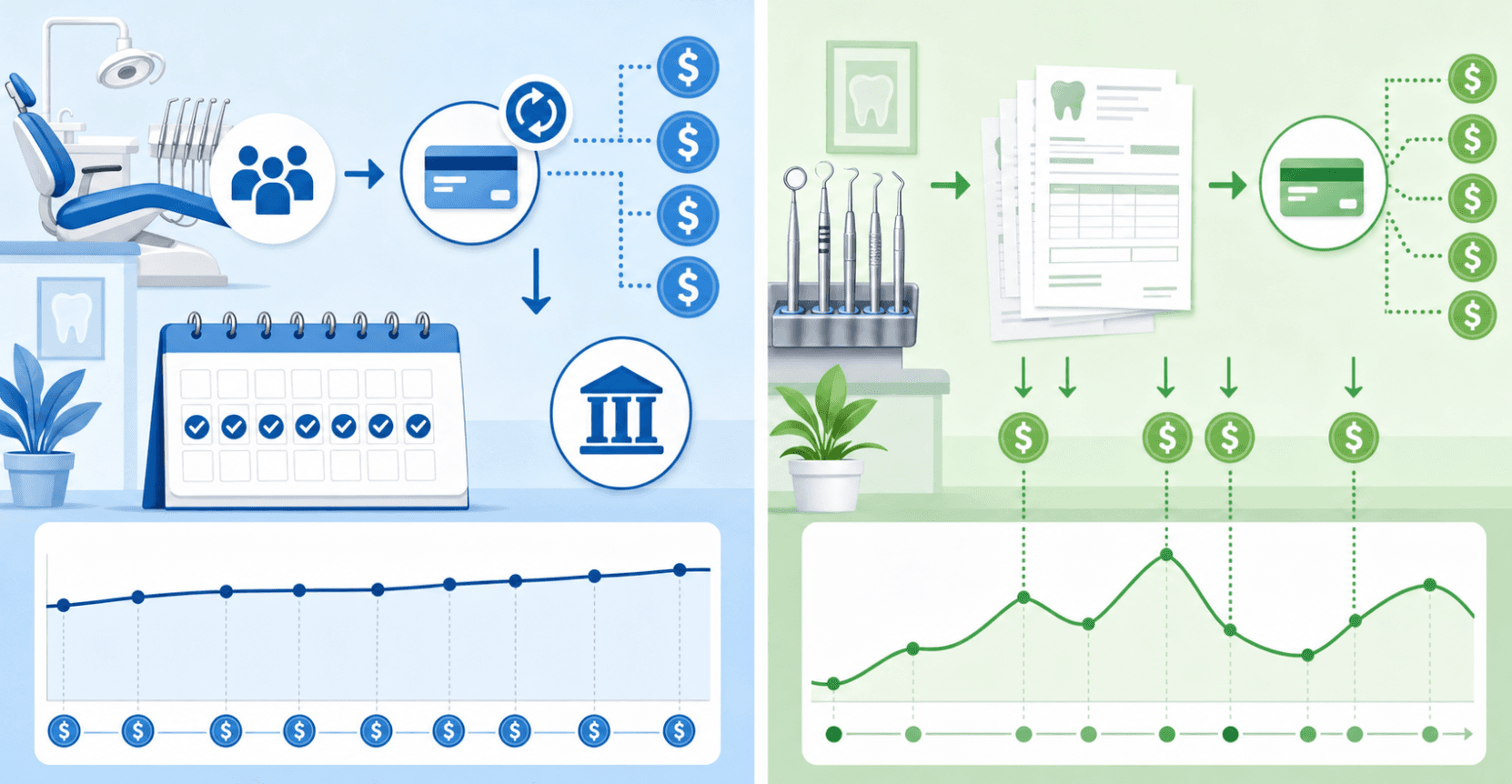

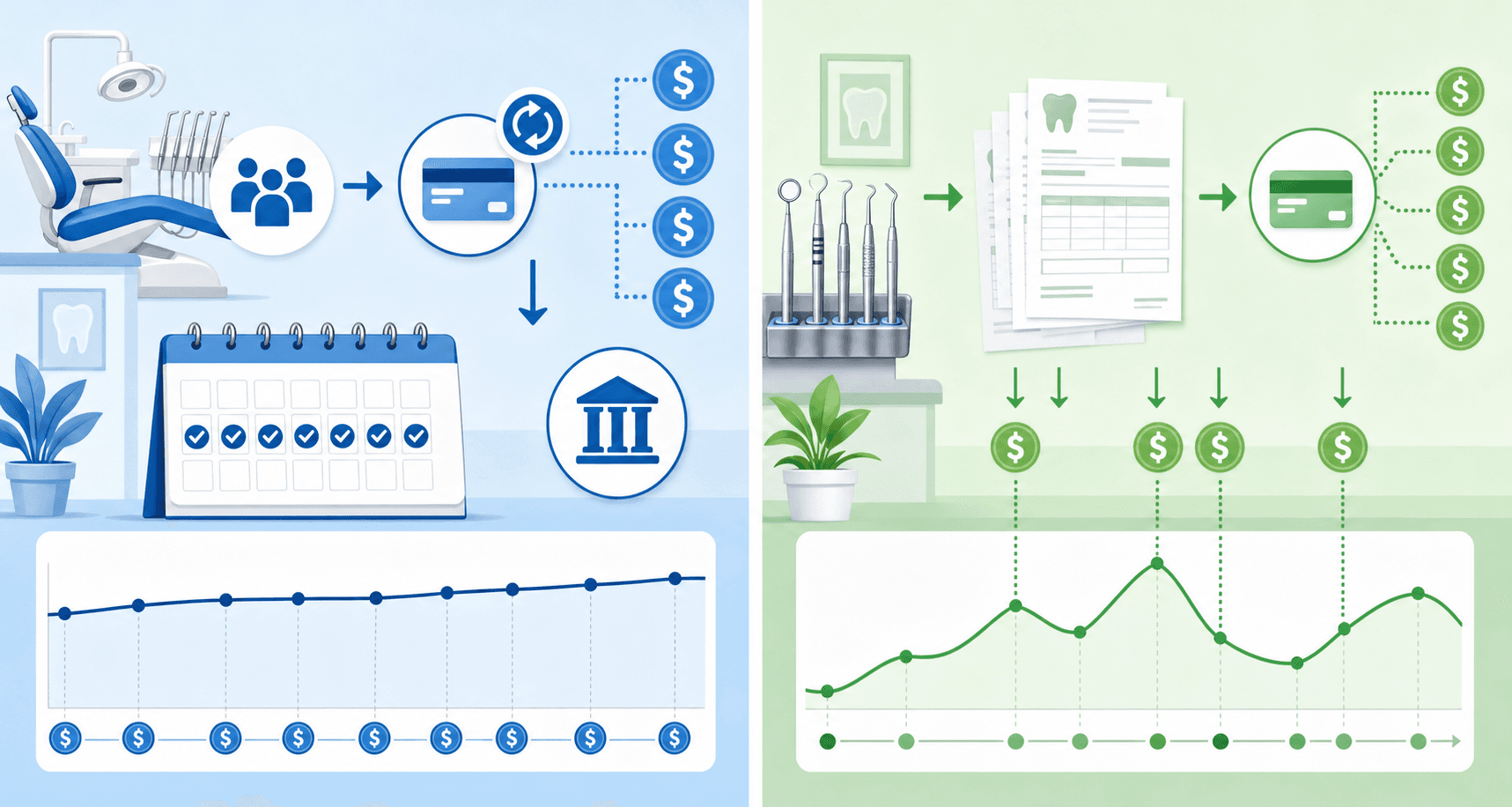

The revenue math under each model behaves differently. Under a DPPO, every procedure becomes a claim paying a contracted percentage of the negotiated fee, with cash flow lagging 14 to 45 days behind the visit.

DHMO revenue arrives in two streams: a monthly capitation check whether chairs sit empty or full, plus procedural copays at a guaranteed schedule. Predictable, but per-patient yield often falls short of your usual fee.

| Factor | DPPO | DHMO |

| Revenue trigger | Claim per procedure | Monthly capitation per member |

| Reimbursement basis | Contracted fee schedule | PMPM plus copay schedule |

| Cash flow timing | After claim adjudication | Recurring monthly |

| Revenue ceiling | Tied to production volume | Capped by enrollment |

High-production offices generate more top-line revenue per patient under PPO contracts, but can fall behind on AR. Capitation rewards tight scheduling and recall discipline, since unused capacity still pays.

Network Participation Requirements and Credentialing Considerations

Joining either network means clearing the same credentialing gauntlet, and the timeline rarely cooperates with revenue planning. Most carriers take 60 to 180 days to verify a new provider before paying in-network rates, per provider credentialing timeline data.

What carriers verify

- Active CAQH profile with current attestation

- State dental licensure and DEA registration, where applicable

- Education, residency, and board certifications

- Malpractice coverage at the carrier's minimum limits

- Individual and group NPI numbers, plus W-9 and tax ID

Strategic network selection

DPPO panels expand your patient pool but lock you into fee schedules 20 to 40 percent below UCR, per PPO fee schedule analyses. DHMO contracts deliver capitation income but cap per-procedure revenue. Audit local demographics first: a Cigna DHMO-heavy market rewards that contract, while PPO-dense zip codes favor Aetna or BCBS panels.

Claims Submission and Processing Workflow Differences

Capitated DHMO visits skip the claim entirely for covered preventive and basic services: the monthly PMPM check already settled it. Your front desk logs the encounter, collects any copay from the carrier's fixed schedule, and moves on. Only specialty referrals or non-covered upgrades generate a claim.

DPPO visits trigger a full claim cycle for every procedure. Submit electronically with CDT codes, tooth and surface notation, and narratives where required. Payers adjudicate within 14 to 30 days, while paper submissions can stretch to 45 days or more.

Workflow load by plan type

- DHMO: minimal claim volume, heavy roster reconciliation against monthly eligibility files

- DPPO: high claim volume, line-item posting, EOB matching, and denial follow-up on every visit

Patient Eligibility Verification and Coverage Confirmation

Verification prevents or creates billing problems. DHMO eligibility hinges on one question: is this office listed as the member's assigned primary dental provider? If not, the visit is uncovered, and the capitation check never reflects them. Cigna and Aetna let members switch assignments by the first of the following month, so a same-day booking under the wrong PCD will not pay.

DPPO verification differs. Confirm active coverage, in-network status of every treating provider, remaining annual maximum, deductible met, frequency limitations on prophylaxis and bitewings, and missing tooth or replacement clauses.

Front-office checklist before the chair

- Pull a real-time eligibility response through your clearinghouse or payer portal

- Confirm PCD assignment for any DHMO patient and document the effective date

- Verify referral authorization for DHMO specialty visits before treatment begins

- Capture remaining maximum, deductible status, and waiting period flags for DPPO patients

- Save the eligibility response in the patient record for denial defense

Skipping any step turns a clean visit into a write-off six weeks later.

Documentation and Attachment Requirements for Major Procedures

Major procedures are subject to scrutiny from both plan types, but the paperwork burden differs. DPPO carriers want clinical proof tied to the CDT code on every crown, bridge, implant, or perio claim. DHMO carriers care less about post-treatment documentation and more about pre-treatment referral authorization from the assigned PCD.

DPPO attachments by procedure category

| Procedure | Required attachments |

| Crowns (D2740-D2752) | Pre-op periapical or bitewing, narrative on cusp coverage or fracture |

| Bridges (D6240-D6245) | Full-mouth or full-arch film, perio charting, and missing tooth date |

| Implants (D6010, D6056-D6059) | CBCT or full-arch, surgical narrative, treatment plan |

| SRP (D4341-D4342) | Recent periodontal chart with pocket depths, bone loss imaging |

DHMO authorization flow

- Submit a referral request through the carrier portal before scheduling

- Include the treating specialist's NPI and anticipated procedure codes

- Wait for written authorization (5 to 10 business days) before booking

- Without authorization on file, the specialist visit reverts to out-of-pocket

Missing a perio chart on a D4341 or pre-op film on a D2740 triggers a request-for-information loop, adding two to four weeks to payment.

Cost Structure Implications: Deductibles, Annual Maximums, and Patient Collections

Patient financial responsibility looks nothing alike across these plans, and your collections script needs to reflect that. DHMO members owe a fixed copay pulled from the carrier's schedule: $0 for a prophy, $65 for a posterior composite, $300 for a PFM crown. No deductible, no annual cap.

DPPO patients have annual deductibles of $25 to $75 and annual maximums of $1,500 to $2,000 that reset each plan year. Once that ceiling is reached, every additional procedure is billed at 100 percent patient responsibility.

What to tell patients before treatment

- DHMO: quote the exact copay from the carrier fee schedule, due at the visit

- DPPO: quote the estimated patient portion after deductible and coinsurance, and flag the remaining annual maximum

- Both: get signed financial agreements for treatment exceeding $500 in patient responsibility

Front desk staff who quote a DPPO crown without checking the remaining maximum hand the practice a collections problem dressed up as a treatment plan.

Out-of-Network Billing and Reimbursement Scenarios

Out-of-network billing splits cleanly along plan type. A DPPO patient at a non-contracted office still receives partial reimbursement at the carrier's UCR or a percentile of allowable charges, with the practice free to balance bill the difference. DHMO patients walking in cold are uncovered entirely, save for documented emergencies.

Practical OON scenarios

- DPPO patient, OON visit: collect full fee at time of service, submit the claim as a courtesy, assign benefits to the patient

- DHMO patient, OON visit: collect full fee, no claim filed, document any emergency exception

- DPPO patient mid-treatment when the contract terminates: finish under continuity-of-care provisions where offered

Staying fee-for-service preserves UCR pricing but shrinks the addressable pool in PPO-saturated zip codes.

Impact on Practice Valuation and Buyer Perception

Payer mix shapes the price tag the day you list. Buyers and DSO acquirers model EBITDA off collections per patient. DHMO-heavy practices often collect $150, $250 per visit, while fee-for-service practices can charge $350, $500 or more, and that gap compresses the EBITDA multiples buyers apply, pushing valuations toward 3-4x instead of the 6-7x that balanced or fee-for-service practices command, per practice transition analyses.

How payer mix moves the multiple

- Heavy DHMO concentration: lower per-patient revenue caps the top line, pulling multiples toward the low end

- 60 percent-plus PPO with discounted fee schedules: buyer's discount for renegotiation risk

- Balanced PPO with fee-for-service above 25 percent: commands premium multiples

- Out-of-network practices: highest valuations, smallest buyer pool

If exit sits five to ten years out, audit contracts annually and drop the worst-paying PPO panels before listing.

Automating Insurance Billing Workflows With AI-Powered Solutions

PPO participation multiplies claim volume, and claim volume multiplies posting labor. Lassie's AI retrieves EOBs from payer portals, reads them, and posts line-item payments into Dentrix, Eaglesoft, or Open Dental against your contracted fee schedules. Downgrades, overpayments, and fee mismatches get flagged instead of being buried.

Where automation absorbs the PPO workload

- Auto-posting against contracted allowables, with practice-specific rules for write-offs and adjustments

- Real-time bank reconciliation so EFT deposits match posted EOBs to the cent

- Centralized search across every EOB for audit defense and patient inquiries

- Automated secondary claim filing for Open Dental practices accepting dual coverage

You can take on another PPO panel without adding another biller.

Final Thoughts on Dental Insurance Plan Structures

Network participation is a trade: you accept lower fees or capped revenue in exchange for patient flow. DHMO keeps billing simple and cash flow steady, but PPO contracts give you more per-patient upside if you can manage the claim volume. Take a hard look at what each contract actually pays after you subtract the administrative cost of collecting it, then decide which panels earn their spot on your roster. If PPO claim volume is eating your billing team's time, book a demo with Lassie to see how AI posting cuts that overhead without adding headcount.

FAQ

DHMO vs PPO: Which dental plan type is better for billing?

DPPO contracts generate higher per-patient revenue through fee-for-service reimbursement but create heavier claim volume and AR lag, while DHMO delivers predictable monthly capitation with minimal claims but caps per-patient yield. Your billing preference depends on whether you value production-based top-line growth or cash flow predictability with lower administrative overhead.

Can I accept a PPO dental insurance patient if my credentialing is still pending?

No. Most carriers take 90 to 180 days to complete provider credentialing, and claims submitted before your effective network date will be processed at out-of-network rates or denied entirely. Wait for written confirmation of your in-network status before scheduling PPO patients.

What happens to a DHMO patient if they come to my practice but I'm not their assigned primary dental provider?

The visit is uncovered, and the monthly capitation check will never reflect that patient. DHMO members must formally switch their assigned primary dental office through the carrier portal before their practice can bill the plan, and that assignment change typically takes effect on the first of the following month.

Cigna dental PPO vs DHMO for high-production offices?

Cigna DPPO pays a contracted percentage per procedure with no revenue cap, making it better for high-volume practices that can absorb the claims workload and 14-to-30-day payment lag. Cigna DHMO pays a fixed monthly capitation regardless of visits, which rewards tight recall schedules but limits per-patient revenue, less attractive when production volume is high.

How does the PPO payer mix affect the practice sale price?

Buyers discount practices with 60 percent-plus PPO concentration because discounted fee schedules compress collections per patient and carry the risk of renegotiation. Practices maintaining 25 percent or more fee-for-service alongside balanced PPO contracts command premium multiples, while heavy DHMO concentration lowers valuations due to capped per-patient revenue.